12.11.2024

ESG regulations and standards - what are they and what advantage can they give?

Key information:

- The European Union has introduced regulations to include non-financial factors in corporate reports.

- The CSRS Directive extends ESG reporting obligations to some 50,000 companies in the EU and requires more detailed reporting of non-financial performance compared to the earlier NFRD.

- The CSRS directive will be phased in from 2025 to 2029.

- The European Sustainability Reporting Standards (ERSR) unify the rules for creating ESG reports.

- Sector Standards and Simplified Standards for SMEs are expected to be released in the near future.

- By implementing the new ESG standards, companies can expect to have an advantage over their competitors when bidding for contracts or raising capital. Taking ESG categories into account will allow companies to make better strategic decisions.

Details below!

Differences between regulations and standards

Although the acronym ESG itself has been on the market since 2004 and is part of the 2015 UN-introduced ESG Agenda 2030 and although by definition it touches on aspects such as environmental impact, social issues and corporate governance standards, the lack of global ESG standards has been a huge obstacle for ESG to have real business value.

The European Union, noticing this problem, decided to establish appropriate regulations on business entities regarding ESG reporting. The regulations are supposed to expand the financial statements to include non-financial factors, that is, to expand the responsibilities of business to include sustainability, social and corporate responsibility issues. In turn, the standards address how ESG is to be reported in the reports.

Basic ESG regulations

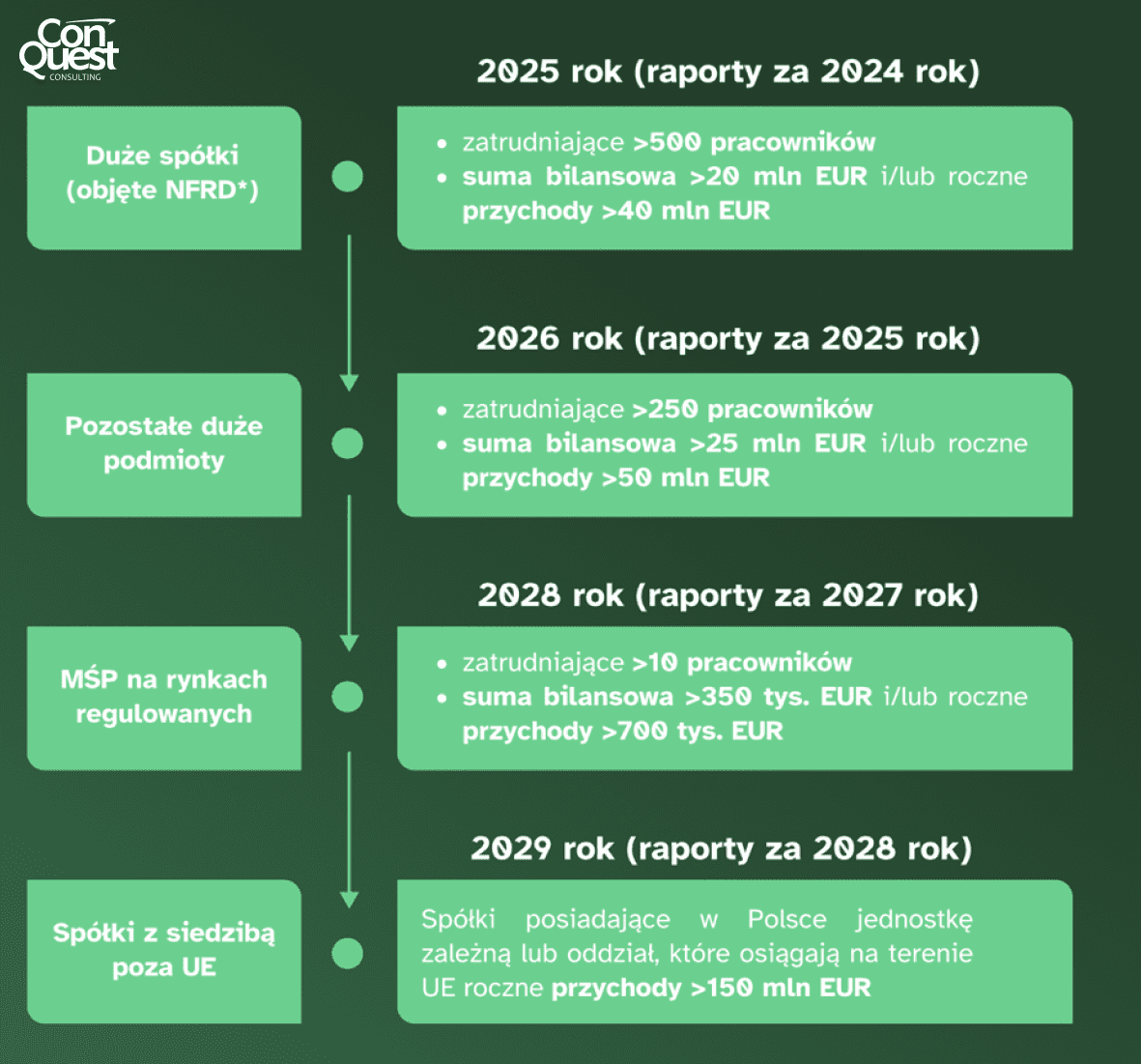

Regulations were introduced in two stages - in 2017 a directive was issued NFRD (English. Nonfinancial Disclosure Reporting Directive), which imposed the obligation to report annual reports and KPIs on public interest entities (PIEs). In doing so, it did not impose a specific reporting model, instead encouraging the use of already existing frameworks, such as the following Global Reporting Initiative (GRI) or Integrated Reporting Framework (IRF). By law, 150 of the largest companies in Poland were covered, and 11,700 in the entire European Union.

The NFRD has undoubtedly contributed to improving the availability of ESG information among companies in the EU. However, many stakeholders (including investors) expressed concerns that the information disclosed by companies was insufficient and difficult to compare due to the lack of a common, unified ESG reporting standard. In addition, it was necessary to align the NFRD's requirements with provisions introduced at later stages as part of the EU Sustainable Finance Strategy, i.e. the EU Taxonomy and SFDR.

In its place, therefore, the directive was introduced CSRD (English. Corporate Sustainability Reporting Directive). What makes it stand out on the map of EU regulations? The CSRD strongly expands the scope of non-financial reporting, increasing the number of entities subject to ESG reporting and expanding the scope of sustainability information. It applies to some 50,000 companies listed in the EU or with significant operations in the Union, regardless of where they are headquartered. Under the CSRD, such companies are required to report non-financial performance more extensively than was required under the previous legislation. The directive, in order to allow time for the implementation of ESG in the reports of business entities, will be introduced gradually:

In order to pursue the sustainable development goals set by the Paris Agreement (i.e., aiming for climate neutrality by 2050 at the latest) and Agenda 2030, the European Union has introduced a EU taxonomy, which aims to standardize the classification system for companies' sustainability reporting standards. The EU taxonomy determines whether a company can be defined as environmentally sustainable if it makes a significant contribution to one of the 6 objectives of environmental issues:

- Mitigating climate change

- Adaptation to climate change

- Sustainable use and protection of water and marine resources

- Transition to a closed loop economy

- Pollution prevention and control

- Protection and restoration of biodiversity and ecosystems

At the same time, the company must not harm any of its other goals and must operate in accordance with minimum guarantees, such as OECD guidelines, UN principles and ILO core conventions.

Main ESG standards

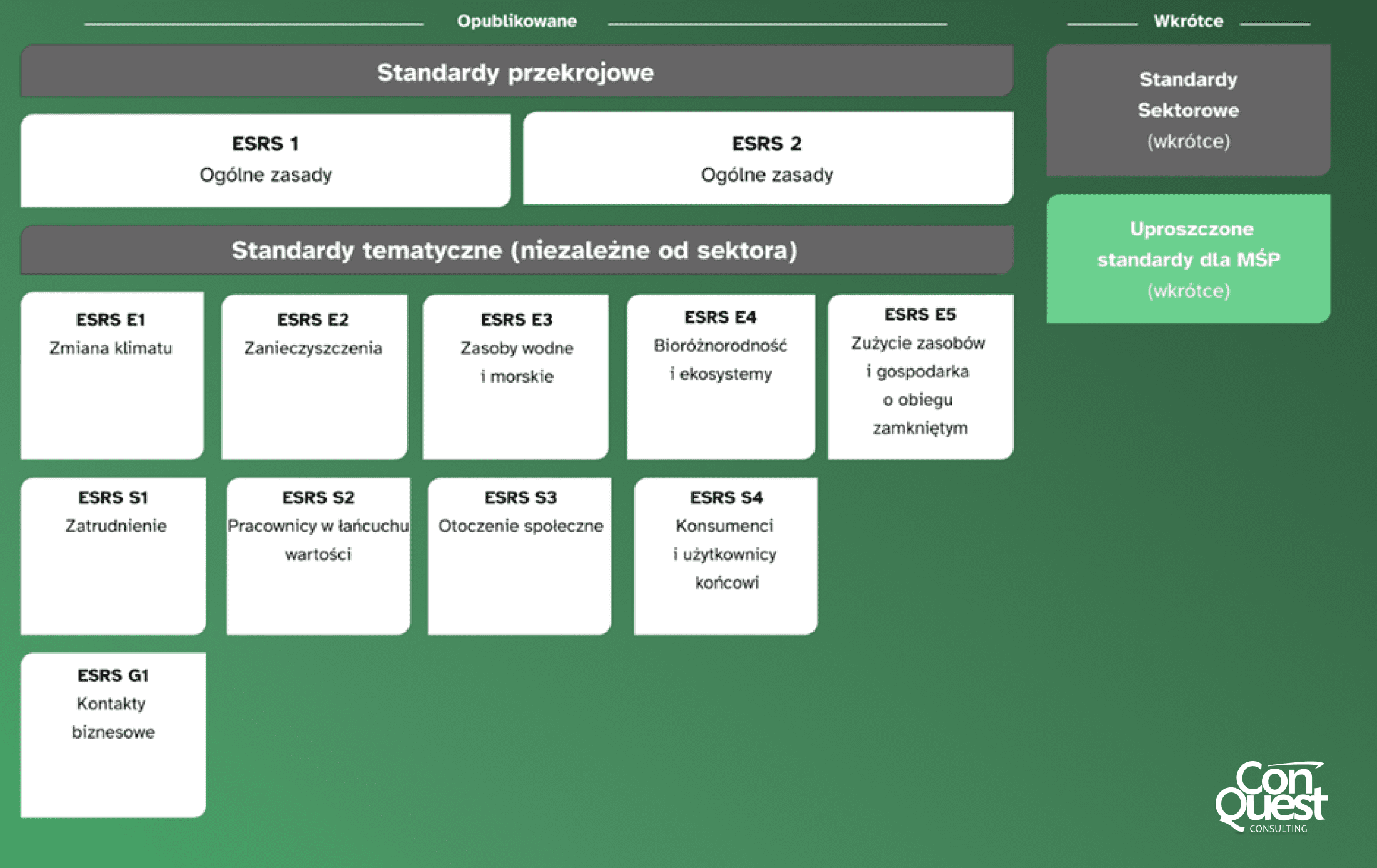

At the end of July 2023, the European Commission approved the European Sustainability Reporting Standards (ESRS) and thus obtained an officially sanctioned set of ESG reporting guidelines. The ESRS unify the rules for creating reports, which were previously diverse and inconsistent. The entire document consists of 12 documents, including two cross-cutting ones discussing the basics of ESG standards and 10 focusing on thematic standards.

The European ESG reporting standards contained in the ESRS link to the TCFD i ISSB, through a similar standards structure, to ensure interoperability of global ESG standards. The requirements included in the ESRS apply to the areas:

- governance (GOV),

- strategy (SBM),

- Impact, Risk and Opportunity (IRO),

- indicators and targets.

In addition, thematic standards will apply, but not all of them will apply to all companies, due to the nature of different industries. Information disclosed by companies will be evaluated for materiality. Only topics deemed material should be included in sustainability reports. For topics that are deemed not material, the company should only explain how it reached this conclusion.

- Dual materiality

The principle of dual materiality in the context of ESG (Environmental, Social, and Governance) reporting is to identify material ESG issues from two perspectives: financial and impact. Companies subject to CSRD are required to describe these issues so that the results of the materiality assessment translate into both business strategy and the identification of ESG topics in sustainability reports. Financial materiality assesses the impact of ESG on a company's financial performance, such as revenues, expenses, assets and liabilities. Impact materiality assesses the potential impact of a company's operations on the environment and society, both directly and indirectly through the value chain. The dual materiality principle combines these two perspectives, deeming an ESG topic material if it is relevant from the financial side, the influential side or both at the same time, enabling better management of risks and long-term value creation.

- Careful

Sustainability due diligence is the process by which companies identify, prevent, mitigate and account for their actual or potential negative impacts on the environment and people throughout their value chain. The ESRS defines the basic elements of this process, which includes incorporating due diligence into the corporate governance model, sustainable investment strategies, dialogue with affected stakeholders, identifying and assessing negative impacts on people and the environment, actions to prevent negative impacts, and monitoring the effectiveness of implemented actions and their communication. Each of these steps is linked to specific disclosures according to ESRS reporting standards, which help companies fulfill their sustainability responsibilities, ensuring transparency and accountability to stakeholders.

- Value chain

ESRS standards require companies to use a value chain approach to ESG disclosure. As a result, companies need to be aware of the activities and processes they impact during material sourcing, production, distribution, and customer use and post-use of products. The assessment of material impacts, risks and opportunities should cover the entire value chain to ensure a comprehensive approach to managing ESG impacts. Reporting in this regard should be consistent with the results of the due diligence process, as well as meet the requirements of the ESRS thematic standards. If obtaining information at earlier or later stages of the value chain is difficult, companies should explain the steps they took to obtain the information and the obstacles they encountered. In this way, companies can provide precise and relevant information on their entire environmental and social impact.

The future of regulation and standards

In the future, ESG reporting in accordance with the CSRD and ESRS reporting standards, is expected to be a boost to global sustainability standards, but also a tool for corporate development. European non-financial reporting standards create a universal system for comparing entities, thereby increasing transparency and trust in the market. Companies, thanks to the benefits of reporting, will have a better chance in tenders where a high ESG rating is required. For example, banks and financial institutions are increasingly requiring ratings at appropriate levels as a condition for granting credit.

ESG benefits such as ensuring sustainability by turning away from solutions that negatively impact the environment, as well as by improving equity and social responsibility and good governance practices, mean that modern companies are increasingly incorporating ESG into their strategies. In the future, ESG regulation will continue to evolve to meet the growing demands and global challenges included in Agenda 2030, such as climate neutrality and human rights protection.

Through these regulations and standards, companies can better make strategic decisions, manage risks, build trust among stakeholders and contribute to building a sustainable economy.

Gain a competitive edge with the benefits of ESG reporting

Adopting and implementing ESG standards is not only an obligation, but also an opportunity for the long-term success and development of the company in accordance with the principles of the ESG category. Companies that choose to implement these standards gain a competitive advantage, especially in terms of raising capital and participating in tenders requiring high standards of corporate responsibility. At the same time, they contribute to the sustainable development of the economy by minimizing negative environmental impacts and supporting socially responsible practices.

Contact us, to learn more about how we can assist your company in preparing and executing a sustainable development strategy!

Timothy Węzik

See other entries